Most dental practice bookkeeping is built for one purpose: tax compliance. The books close sometime in January, the CPA files in April, and the numbers satisfy the IRS. What they often don’t tell you is whether the practice is actually performing the way you think it is.

That gap tends to be specific. Production looks healthy but collections are flat. Lab fees are rising inside a line that doesn’t show them separately. These aren’t accounting errors — they’re tracking gaps.

This post covers what bookkeeping for dentists should actually track every month — and where the most common gaps tend to appear.

The Production–Collections Gap Is the Number That Matters Most

Production and collections are different numbers, and bookkeeping for dentists has to track both. Treating them as one produces books that look accurate and aren’t.

Production is the full value of the dentistry you deliver — every procedure billed at your fee schedule. Collections is what the practice actually receives after insurance adjustments, contractual write-downs, and patient payments. In a typical dental practice, those two numbers can differ by 10 to 20 percent. Only collections belong on your P&L.

📊 The ADA’s KPI framework sets a target collection rate of 98% of adjusted production — meaning no more than 2% in bad debt.1 Practices running below 95% are leaving measurable revenue on the table every month, and most don’t know it because the gap isn’t being tracked.

Why recording production as revenue distorts everything downstream

When production gets recorded as revenue, every margin calculation in the practice becomes unreliable. The overhead looks lower than it is. Net income looks higher. The numbers satisfy a casual review and mislead a serious one.

The correct approach is to record collections as revenue and track contractual adjustments — the discount written off under a PPO contract — separately from true write-offs, which are uncollectible patient balances. Blending them makes it impossible to evaluate your actual collection rate.

What a widening gap tells you

The spread between production and collections, tracked over consecutive months, is one of the clearest signals in dental practice finance. A widening gap that isn’t explained by a new PPO contract usually points to a collections problem — slow insurance follow-up, aging patient balances, or claims that were submitted and not pursued.

A bookkeeper working between Dentrix or Open Dental and QuickBooks needs to reconcile those two systems every month. Without that reconciliation, the data drifts — and the gap between them is exactly what surfaces in an insurance audit.

EOB Reconciliation: Where Dental Practices Lose Money Quietly

EOB reconciliation — matching Explanation of Benefits documents to actual deposits — is one of the most dental-specific parts of dentist bookkeeping, and one of the most commonly skipped.

The basic problem: you submit a claim for $800. The EOB says the insurer paid $600. The deposit in your account shows $550. Each discrepancy seems manageable. Across a practice doing $1.2 million in collections, they compound quickly.

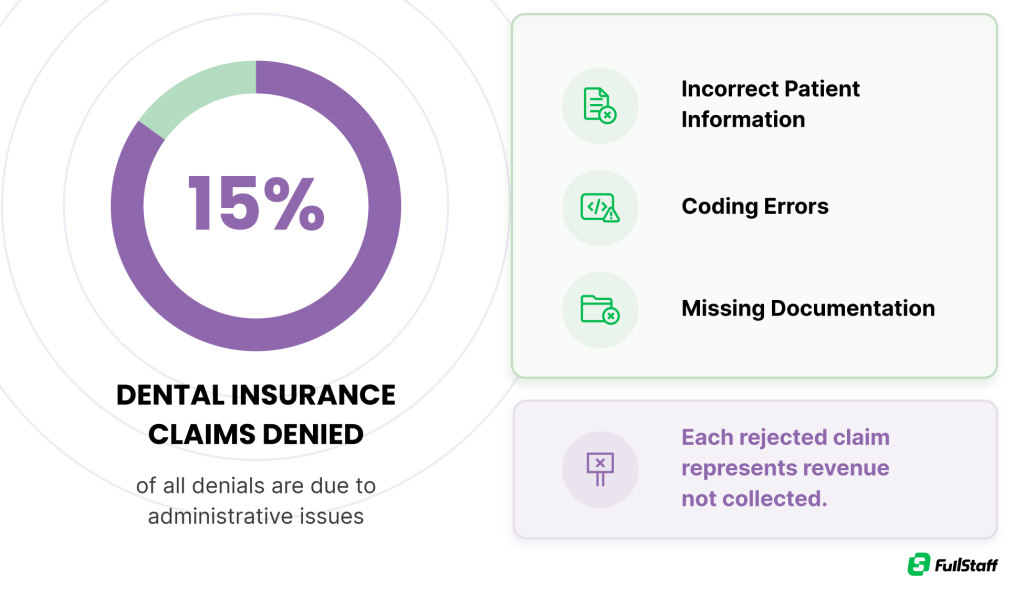

📊 About 15% of dental insurance claims are denied, making accurate coding, complete documentation, and proper claim submission essential for maintaining steady cash flow and reducing avoidable payment delays.2

Why insurance ERA batches create reconciliation problems

Electronic remittance advice often arrives bundled — one deposit covering payments for multiple patients across multiple dates of service. Without line-item allocation, those payments land as a lump sum and individual claim underpayments go unnoticed until the appeal window has closed.

Dental collections reconciliation requires matching each carrier payment to the individual claim and patient — not just confirming that the deposit hit the bank.

Each carrier needs to be tracked separately

Delta Dental, MetLife, Cigna, Aetna, and United Concordia each have different claim processing windows, fee schedule interpretations, and downcoding patterns, as Teero’s dental payment reconciliation guide details.3 Treating them as a single insurance income line in QuickBooks makes it impossible to identify which payers are underpaying consistently or where claims are aging past the point of appeal.

A bookkeeper who matches deposits to bank statements is doing bank reconciliation. That’s not the same as EOB reconciliation. A dental practice needs both.

A dental bookkeeper who can’t tell you which carrier is consistently short-paying isn’t doing the full job.

Expense Tracking Built for a Dental Practice

A generic chart of accounts doesn’t distinguish between dental supplies, lab fees, and equipment. This is one of the clearest places where bookkeeping for dental practices differs from standard small-business accounting — and where the wrong setup quietly distorts the numbers.

Lab fees deserve their own line item

Lab fees are a variable cost tied directly to case mix. They should be tracked as a percentage of collections and matched against the cases that generated them. If those fees are buried in a general dental supplies category, you can’t tell whether a shift in case mix is affecting your margins.

The benchmark: lab fees at 5–8% of collections is considered healthy. Above that, the case mix or pricing structure deserves a closer look.

📊 Dental Economics, citing guidance from the Academy of Dental CPAs, benchmarks dental supplies at 6% of collections and lab fees at 8% — with staff costs (excluding owner compensation) not to exceed 28%, and a target of 24–26%.4 If your books don’t break each line out separately, you can’t tell which category is pulling overhead in the wrong direction.

Dental supplies: the 7% benchmark only works if it’s tracked

Dental supplies average around 7.3% of collections across the industry, with higher-performing practices keeping that figure below 7%. A bookkeeper who reports supplies as a flat dollar amount rather than as a percentage of collections makes that benchmark useless — because a $7,000 supplies month looks completely different in a $70,000 collection month versus a $100,000 one.

Equipment belongs on the balance sheet, not in supplies expense

Any equipment purchase over $2,500 should be recorded as a fixed asset and depreciated over time, not expensed into dental supplies. Coding a $15,000 operatory chair to a supplies line overstates overhead in the month of purchase, distorts monthly expense comparisons, and removes the depreciation benefit from the financials.

Hygiene Production: What It Tells You When It’s Tracked Separately

Hygiene typically represents 25–35% of a dental practice’s total production. When that contribution isn’t tracked separately from doctor production, you’re managing the department without a financial picture of it.

Hygiene revenue as a percentage of total production

The hygiene production percentage is a management metric as much as a financial one. A drop in hygiene’s share of production — without a corresponding increase in restorative production — usually points to a scheduling or utilization issue. Your books have to surface it before you can address it.

Provider-level production tracking is one of the core outputs of a well-run dental financial system. QuickBooks’ class tracking feature can separate hygiene revenue from restorative and cosmetic production, giving you a monthly breakdown that mirrors how the practice actually generates revenue.

Hygiene payroll against hygiene production

Hygienists typically earn 30–40% of their production in compensation. That relationship only makes sense when hygiene labor costs are tracked against hygiene revenue — not folded into a combined payroll total. When the two are blended, a practice running hygiene at 65% utilization looks identical on paper to one running it at 90%.

📊 Dental Economics identifies hygiene production as contributing 25–35% of gross practice production — and sets the salary-to-production ratio benchmark at approximately 33% (hygienists should produce roughly three times their wages).5 When that ratio climbs toward 40% or above, excessive downtime is usually the cause, and it’s the kind of number the books should be surfacing monthly.

If your hygiene department’s numbers aren’t broken out in your books, you’re running it on gut feel.

Owner Compensation: The Bookkeeping Item Most Dental Practices Get Wrong

Owner compensation is where dental practice bookkeeping most often breaks down — and the errors here affect both the accuracy of the financial reports and the practice’s tax position.

Owner draws don’t belong on the P&L

A draw is an equity withdrawal, not a business expense. Recording it on the Profit and Loss statement suppresses apparent profit, understates overhead as a percentage of collections, and makes every margin calculation unreliable. Draws belong on the balance sheet as a reduction to the owner’s equity.

This distinction matters practically: if your P&L is being used to evaluate the practice for a sale, a loan, or an associate buy-in, draws recorded as expenses are a problem that surfaces in due diligence.

Salary versus distributions in an S-corp dental practice

Most dental practices operate as S-corps, where the owner is required to take a reasonable salary before pulling distributions. The split directly affects payroll tax liability. The IRS pays close attention to practices where distributions are disproportionately high relative to salary. A bookkeeper’s job is to track both accurately every month, so the compensation structure can be reviewed before a filing — not during one.

📊 The University of Illinois Tax School identifies S-corp reasonable compensation as “one of the areas of low-hanging fruit for IRS auditors” — noting that the IRS has authority to reclassify distributions as wages and assess back payroll taxes, accuracy penalties, and interest when owner compensation is disproportionately low relative to distributions.6

Associate compensation tracked separately from owner compensation

In a multi-doctor practice, blending owner and associate payroll into a single line makes provider-level profitability analysis impossible. The ADA’s guidance on dentist compensation illustrates how associate pay is calculated on an entirely different basis from owner income — production percentages, collection rates, plan adjustments — which is exactly why each category needs its own line in the books.7

Owner compensation recorded correctly keeps the financials useful for something beyond tax filing.

Why Bookkeeping for Dentists Needs a Monthly Close

A dental practice managed on quarterly books is making staffing, supply ordering, and fee schedule decisions on data that’s 60 to 90 days stale. The monthly close is what keeps the financial picture current enough to use.

Reconciling the practice management system to QuickBooks

Dentrix, Open Dental, and Eaglesoft each hold production and collections data that QuickBooks doesn’t receive automatically. Without a monthly reconciliation between those systems, the books drift from the practice’s actual financial activity. That drift is gradual — which is why it often goes unnoticed until the gap is significant.

The reconciliation should confirm that collections recorded in the practice management system match deposits in the bank, that adjustments are categorized correctly, and that any discrepancy between production and deposits is explained.8

The monthly financial snapshot a dental practice needs

Six numbers cover most of the ground: net collections rate, overhead percentage, lab fees as a percentage of collections, hygiene production percentage, accounts receivable aging, and owner compensation balance. Dental practice overhead typically runs 60–65% of collections, excluding owner compensation.9 Overhead above 70% signals a problem that a monthly review should have caught earlier.

📊 2740 Consulting’s dental claims data shows the average annual claim collection rate for dental practices sits at just 84% — well below the 98% target experts recommend.10 Most practices running below that threshold don’t know it because the gap between what’s billed and what’s collected isn’t being measured month to month.

When these numbers arrive monthly, they’re management tools. When they arrive in April for the prior year, they’re a history report.

Monthly books aren’t a tax requirement — they’re a decision tool.

The Difference Between Compliance Books and Management Books

Bookkeeping for dentists works best as a management function, not a compliance one. The difference shows up in three areas: whether production and collections are tracked separately and reconciled monthly, whether the chart of accounts is structured for a dental practice rather than a generic business, and whether the monthly close connects the practice management system to the accounting software.

A bookkeeper who handles these correctly doesn’t just keep the IRS satisfied — they give you a clear picture of how the practice is performing month over month.

If you want to see what that looks like in practice, FullStaff’s bookkeeping services for dental practices include a monthly financial dashboard built around the metrics covered here. You can also review how the onboarding process works if you’re evaluating whether a dedicated bookkeeper makes sense for your practice.

Frequently Asked Questions (FAQs)

What’s the difference between production and collections in dental bookkeeping?

Production is the full value of services billed at your fee schedule. Collections is what the practice actually receives after insurance adjustments and patient payments. Only collections belongs on your income statement — recording production as revenue inflates every margin calculation, and the spread between the two, tracked monthly, tells you whether your collection rate is holding or quietly declining.

How should a dental practice track insurance payments and EOBs?

Each payment should be matched to the individual claim and patient — not recorded as a lump deposit. That means comparing the amount billed, the EOB, and the actual deposit, and flagging discrepancies before the appeal window closes. Delta Dental, MetLife, Cigna, and other carriers each have different processing patterns, so tracking them in separate categories is the only way to identify which payers are consistently short-paying.

What’s a healthy overhead percentage for a dental practice?

Healthy overhead runs 55–65% of collections, excluding doctor compensation — above 70% signals a problem. Track it as a percentage of collections, not a flat dollar figure, so shifts in production volume don’t obscure real cost trends. Payroll typically accounts for 33–34%, dental supplies around 7%, and lab fees between 5–8%.

How should lab fees be categorized in dental practice bookkeeping?

Lab fees should have their own expense line, separate from dental supplies. They’re a variable cost tied directly to case mix — crown and bridge generates lab fees; hygiene and preventive work generally doesn’t. Tracking them as a percentage of collections (benchmark: 5–8%) and matching them to the cases that produced them is the only way to evaluate procedure-level profitability.

What financial reports should a dentist review every month?

The core monthly package: a P&L using collections as revenue, an AR aging report, a production-by-provider breakdown separating hygiene from doctor production, an overhead summary showing supplies, lab fees, and payroll as percentages of collections, and an owner compensation summary. These reports are only useful if the books close monthly — quarterly closes mean the data arrives too late to act on.

What’s the difference between a write-off and an adjustment in dental bookkeeping?

A contractual adjustment is the discount built into your PPO contract — a predictable, negotiated reduction on every insurance claim. A write-off is an uncollectible patient balance removed from accounts receivable. They’re different situations and should never share a category. Blending them makes it impossible to tell whether your collection rate is declining or your PPO mix is shifting.

Can a general bookkeeper handle dental practice books?

A general bookkeeper can manage the transactional layer — reconciliation, categorization, accounts payable. What typically gets missed is the dental-specific work: reconciling the practice management system to QuickBooks, allocating EOB payments at the claim level, tracking hygiene production separately from doctor production, and maintaining a chart of accounts built for dental expense structures. The gap isn’t complexity — it’s familiarity with the reporting a dental practice actually needs.

Let FullStaff Handle Your Bookkeeping

Managing dental practice bookkeeping takes consistency. As your practice grows, so do the transactions, insurance reconciliations, provider payroll entries, and reporting requirements. Meanwhile, your team is focused on patient care — not maintaining the books.

Since 2012, FullStaff has helped businesses maintain organized, reliable financial records through dedicated bookkeeping support. Every bookkeeper holds an accounting degree, follows US GAAP standards, and works as an assigned team member — not a rotating resource.

FullStaff can help with:

- Production and collections reconciliation

- EOB tracking and insurance payment allocation

- Bank and credit card reconciliation

- Transaction categorization and coding

- Accounts payable and receivable tracking

- Monthly close and reporting

- Profit and Loss statements

- Provider-level production reporting

- Catch-up bookkeeping support and more

The process is simple: Complete a quick kickoff form so the team can understand your practice and workflows, meet with FullStaff to discuss your goals and reporting needs, and get matched with a dedicated accounting professional who helps organize your bookkeeping processes from day one.

References:

- ADA Measuring Success

- Dental Insurance Claim Statistics

- How to Reconcile Dental Payments: Insurance and Patient

- Tracking dental practice overhead and what the results mean

- The successful hygiene department: Understanding the numbers

- IRS Audit Issue – S Corporation Reasonable Compensation

- Dentist compensation: what every dental associate should know

- What Is Dental Accounting? A Guide

- Dental Practice Overhead: Cost Breakdown, Benchmarks, and Insights

- Dental Insurance Claim Statistics