Real estate bookkeeping rarely feels urgent until something goes wrong. Commission checks arrive as net deposits, expenses end up on different cards, and tax season quickly becomes a scramble. For brokers handling earnest money, trust-account compliance adds even more responsibility.

Accurate books are part of running a professional real estate business. The same bookkeeping mistakes appear in firms of every size, and small errors can quickly turn into costly problems.

Commission-based income makes bookkeeping easy to delay. Large, irregular deposits can hide errors for months. That’s why many agents turn to real estate bookkeeping services only after those mistakes have already cost them money. Here are the seven most common ones and how to avoid them.

What Clean Agent Bookkeeping Actually Looks Like

Good bookkeeping for real estate agents comes down to a handful of habits, kept up every month:

| A dedicated business checking account and card, with zero personal spending mixed in |

| Every commission recorded at gross, with the split, referral fees, and transaction fees itemized |

| Bank accounts, credit cards, and the commission ledger reconciled against closing statements monthly |

| A mileage log that runs all year instead of being rebuilt from memory in March |

| A fixed percentage of every commission check set aside for quarterly estimated taxes |

| Contractor payments tracked as they happen, so 1099-NEC filing in January is a formality |

| Trust funds, where applicable, held in a designated trust account and reconciled monthly |

None of this is complicated. The challenge is consistency, not complexity.

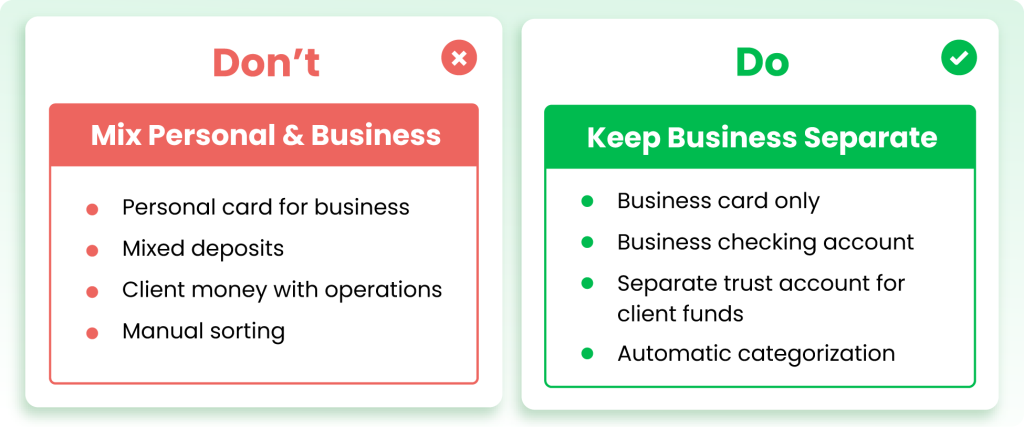

Mistake #1 — Running the Business Through Personal Accounts

The staging invoice goes on the personal card because it was the one in the wallet. Groceries end up on the business card the following week. Six months later, no statement tells a clean story, and every line has to be sorted by memory.

The cost shows up twice. Deductions get missed because business charges hide inside personal statements. And if the IRS ever looks, personal spending claimed as business expense is the first thing an examiner pulls apart.

For brokers, the same instinct becomes a license problem. Client funds held in a brokerage operating account, or earned commissions left sitting in the trust account, both count as commingling. State regulators treat this as a compliance failure, and most require monthly trust-account reconciliation by rule.

📊 The California DRE lists trust fund account and record-keeping violations, including commingling client funds with business or personal accounts, first among the most common enforcement violations it acts against.1

The fix costs nothing: one business checking account, one business card, and a rule that every business dollar touches them.

Mistake #2 — Recording the Net Deposit Instead of the Gross Commission

| Closing #1523 May 15, 2026 |

| Sale Price | $550,000 |

| Gross Commission | $11,000 |

| Broker Split (30%) | -$3,300 |

| Referral Fee | -$600 |

| Transaction Fee | -$250 |

| Net Deposit | $6,850 |

*Book the gross commission as income. Broker split, referral fees, and transaction fees are expenses. The table above is for illustrative purposes only.

A $9,000 gross commission becomes a $5,600 bank deposit after the broker split, the transaction fee, and a referral payout. Most agents book the $5,600 and move on.

That habit erases the information you actually need. Your true revenue is the gross commission, and the difference between gross and net is your cost of doing business with your brokerage. If you can’t see it, you can’t tell whether your split still makes sense at your current volume, or why two similar closings netted different amounts. It also understates income on paper for any lender reviewing your financials.

The fix is a commission ledger, one row per closing: sale price, gross commission, split percentage, fees taken, referral payouts, net received. Book the gross as income and the deductions as expenses.

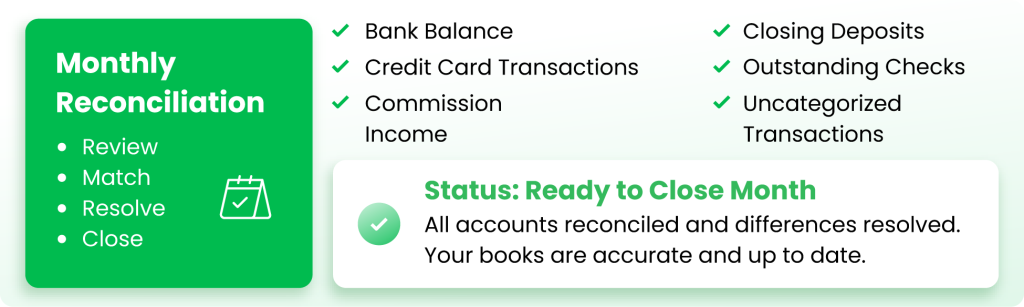

Mistake #3 — Skipping Monthly Reconciliation

Bookkeeping errors don’t announce themselves. A duplicate expense, a closing that never posted, a bank feed that skipped two weeks in June. These survive because nobody checks the books against the bank until tax time, when the person checking is a CPA billing by the hour.

Reconciliation is the checking. Once a month, the bank statement, the credit card statement, and the commission ledger get matched against what the books say, and every difference gets explained. This is the core of what real estate bookkeeping services actually do each month: reconcile, verify, and close, so the numbers can be trusted the other 29 days.

Skip it, and errors compound quietly. Your year-end return gets built on twelve months of unverified numbers. For brokers, monthly trust-account reconciliation is written into most state regulations, and shortages discovered in an audit are treated as violations even when they’re honest mistakes.

Mistake #4 — Losing Deductions You Already Paid For

Agents spend real money running their business, then lose the deduction because nothing captured it.

Based on the 2026 IRS standard mileage rate of 72.5¢ per business mile.2

The same leak runs through smaller categories: lockbox fees, client coffees, staging supplies, MLS dues, photography for listings. Individually forgettable, collectively significant.

📊 REALTORS® reported median business expenses of $9,530 in 2025, with vehicle costs the largest single category, per the NAR 2026 Member Profile.3

This is also where real estate bookkeeping services tend to pay for themselves first. When every expense is captured and categorized monthly, the recovered deductions frequently exceed the cost of the service.

The fix: a mileage app that runs automatically, the business card as the default for every business purchase, and a monthly categorization pass while the charges are still recognizable.

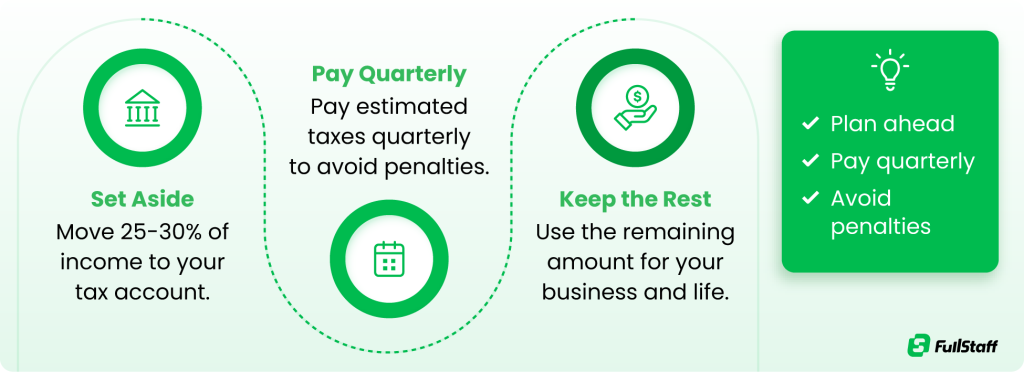

Mistake #5 — Treating Every Commission Check as Spendable

Nobody withholds taxes from a commission check. The full amount hits the account looking like money, and for agents coming from W-2 jobs, this is the most expensive adjustment to miss.

Independent contractors who expect to owe $1,000 or more for the year are required to pay estimated taxes quarterly, using Form 1040-ES.4 Skip the quarterly payments, and the bill arrives in April as a lump sum covering income tax plus self-employment tax, often landing right after a slow winter quarter when the cash isn’t there.

The fix is mechanical. Pick a set-aside percentage, typically 25–30% depending on your bracket and state, and move it to a separate tax account the day every commission lands. Because commission income is uneven, the annualized income method can also reduce penalties in slow-start years.

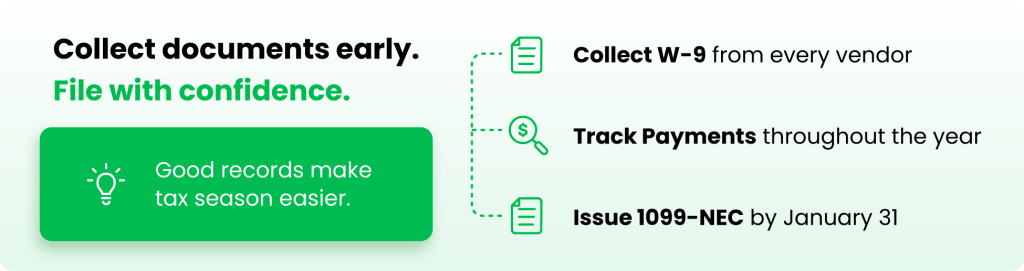

Mistake #6 — Mishandling 1099-NEC Obligations

Agents sit on both sides of the 1099-NEC. Your brokerage issues one to you, and you likely owe them to others: the photographer, the stager, the transaction coordinator, the showing assistant you paid as contractors.

The rules just moved. For payments made through 2025, the reporting threshold was $600 per contractor. Under the One Big Beautiful Bill Act, the threshold rises to $2,000 for payments made on or after January 1, 2026, though several states still require reporting at lower amounts.5 Forms are due to recipients and the IRS by January 31, and filing extensions don’t apply to the 1099-NEC.

On the receiving side, match your brokerage’s 1099 against your own gross commission records. If you kept a commission ledger (Mistake #2), this takes minutes. If you didn’t, you’re trusting their numbers blind.

The fix: collect a W-9 from every vendor at engagement, and track cumulative payments per vendor through the year.

Mistake #7 — Waiting Until Tax Season to Consider Real Estate Bookkeeping Services

The pattern repeats every spring. Twelve months of statements, a shoebox of receipts, a weekend lost to reconstruction, and a CPA charging cleanup rates for work that would have taken a bookkeeper an hour a month. Memory has decayed, receipts have faded, and some deductions are simply gone.

Those hours carry a real price for an agent. Time spent rebuilding the books is time not spent prospecting, showing, or closing.

The threshold question isn’t complicated. If your books are more than a quarter behind, if you can’t state your year-to-date net income within a few thousand dollars, or if last April surprised you, the DIY approach has already failed quietly. Real estate bookkeeping support built for agents and brokerages handles the monthly close, the commission ledger, and the catch-up work in one motion.

Conclusion

Real estate bookkeeping services exist because these seven mistakes keep happening to smart, busy people whose actual job is closing transactions, not categorizing them. The pattern across all seven is the same: what gets skipped monthly gets expensive annually.

Do those three consistently and mistakes four through seven mostly take care of themselves. If the books are already months behind, the fastest path is handing the cleanup to someone who does it every day.

Frequently Asked Questions (FAQs)

Do real estate agents need a bookkeeper?

Not every agent does, but the threshold arrives earlier than most expect. A newer agent closing a handful of transactions can manage with a separate bank account, a mileage app, and an hour a month of discipline. Once volume grows, a team forms, or the books fall more than a quarter behind, the missed deductions, penalty exposure, and lost prospecting hours usually cost more than professional bookkeeping would.

How much does bookkeeping cost for real estate agents?

Dedicated bookkeeping for a solo agent typically runs a few hundred dollars per month, scaling with transaction volume and complexity, and a brokerage with trust accounts pays more than an individual agent. Weigh that against recovered deductions, avoided penalties, and reclaimed hours; you can review what a dedicated bookkeeper costs to put real numbers against your situation.

What expenses can real estate agents deduct?

Common deductible categories include business mileage, MLS and association dues, marketing and advertising, listing photography, staging costs, E&O insurance, license renewals and continuing education, home office expense, client meals (generally at 50%), and fees paid to contractors like transaction coordinators. The requirement across all of them is documentation: a log or receipt tying each expense to business activity.

How should real estate agents record commission income?

Record the gross commission as income, then record the broker split, transaction fees, franchise fees, and referral payouts as itemized expenses, rather than booking only the net deposit. A per-closing commission ledger showing sale price, gross commission, split percentage, fees, and net received preserves your true revenue figure and makes verifying your brokerage’s year-end 1099 straightforward.

Do real estate agents have to pay quarterly estimated taxes?

Yes, in almost all cases. Most agents are independent contractors, and the IRS requires quarterly estimated payments from anyone expecting to owe $1,000 or more for the year, covering both income tax and self-employment tax. Payments are due in April, June, September, and January, and underpaying triggers a penalty even if you settle the full balance at filing.

What is commingling in real estate?

Commingling is mixing client trust funds, such as earnest money deposits, with a broker’s business or personal funds. Depositing earnest money into an operating account counts, and so does leaving earned commissions in the trust account. State regulators treat commingling as one of the most serious license violations, with penalties ranging from fines to license suspension or revocation.

Who gets a 1099-NEC in real estate?

Brokerages issue 1099-NECs to their agents for commission income, and agents issue them to unincorporated service providers they pay above the reporting threshold, such as photographers, stagers, transaction coordinators, and showing assistants. For payments made in 2026 the federal threshold is $2,000, up from $600, though some states still require reporting at lower amounts.

What is the best way to track mileage as a real estate agent?

Use an automatic mileage-tracking app that logs every drive in the background, then classify trips weekly while you still remember them. The IRS requires a contemporaneous record showing date, destination, business purpose, and miles, and a log rebuilt from a calendar months later rarely survives an audit. At the 2026 rate of 72.5 cents per mile, a typical agent’s annual mileage is worth several thousand dollars in deductions.

Can AI replace a bookkeeper for real estate agents?

AI now handles much of the transactional layer — categorizing expenses, matching bank feeds, flagging duplicates — and it does that work faster than a human. It doesn’t replace human judgment on the parts that carry risk: trust-account compliance, gross-versus-net commission treatment, 1099 classification decisions, and catching the error the automation created. The practical setup for most agents is AI-assisted tooling with an experienced bookkeeper reviewing and closing the month.

Let FullStaff Handle Your Bookkeeping

Commission ledgers, agent splits, trust-account reconciliations, and a contractor list that’s ready for 1099 season in January: this is the work FullStaff bookkeepers do every month for agents and brokerages. Want proof before you commit? Ask to see a sample commission ledger and monthly reconciliation report for an agent doing 20+ sides a year.

Since 2012, FullStaff has matched growing businesses with dedicated, degree-qualified accountants who work to US GAAP standards. You get a consistent team member, not a rotating resource.

For real estate professionals, that includes:

- Commission ledger recording and reconciliation

- Trust-account recordkeeping and monthly reconciliation

- Bank and credit card reconciliation

- 1099-NEC preparation support

- Agent split reconciliation

- Catch-up bookkeeping

Here’s how it works: complete a short kickoff form, meet with our team to define what your books need, and get matched with a dedicated accounting professional who learns your business and keeps the close on schedule.

References:

- California Department of Real Estate — Licensee Advisory: Most Common Enforcement Violations (Aug 2025)

- IRS — 2026 Standard Mileage Rate News Release (IR-2025-128

- National Association of REALTORS® — 2026 Member Profile News Release

- IRS — About Form 1040-ES, Estimated Tax for Individual

- Thomson Reuters — State Tax Information Reporting: What Changed in 2025 and What to Expect for 2026