A job-cost report and the project bank balance are two documents that should agree. When they don’t, the discrepancy usually traces back to costs coded to the wrong job, overhead that wasn’t allocated, or retainage lumped into accounts receivable. By the time the gap shows up, the project is already closed.

Construction job costing is designed to close that gap. When it works, it shows which projects are profitable while they’re still running.

This piece covers where job costing breaks down in practice, and what it takes to keep project numbers accurate from the first invoice through the final lien waiver.

📊 57.8% of construction firms fail within ten years. 16.1% don’t survive the first.1 Job-level financial visibility is one of the clearest differences between firms that scale and those that don’t.

What Construction Job Costing Actually Tracks

| Job costing assigns every expense to the correct project and cost code. |

| Cost codes compare estimated costs with actual spending by category. |

| The WIP schedule shows the financial status of every active project. |

| Retainage is a receivable, not cash, and must be tracked separately. |

| Allocate overhead to each job for accurate profit margins. |

| The percentage-of-completion method relies on accurate job cost data. |

| Real-time job costing reveals the actual profit margin on every project. |

The challenge isn’t setting it up. It’s keeping it accurate while the project is still running.

Why Most Job-Cost Reports Are Already Wrong by Mid-Project

The gap between billed and earned

Progress billing doesn’t always match earned revenue. A contractor can bill 60% of a contract value and have earned 40% based on actual work completed. When that difference isn’t tracked, the books record income that hasn’t been earned yet.

The reverse is underbilling: work completed but not yet invoiced, which understates revenue and makes the business look less profitable than it is. Lenders and surety companies flag large overbilling positions as a risk signal. Both distort every financial decision made downstream.

When slow cost coding becomes a margin problem

Costs coded a week late don’t just affect the accounting. They affect the WIP schedule, which affects the percentage-of-completion calculation, which affects how much revenue gets recognized that month. A project that’s 60% complete in the field may only be 48% complete in the system.

Delayed cost coding is one of the most consistent reasons job-cost reports look clean at month-end and then show a loss at closeout. The costs were always there. They just weren’t attached to the job yet.

How Overhead Allocation Errors Undermine Every Bid You Write

What actually counts as overhead in construction

Overhead includes every cost not directly attached to a specific project: insurance, vehicle expenses, equipment depreciation, office salaries, software subscriptions, facilities costs. Every job has to carry its proportional share of those costs. When they aren’t allocated, net margin absorbs the hit instead of the individual project where it belongs.

Most contractors understand this in principle. Fewer apply it consistently in practice.

The flat-percentage trap

A single overhead rate applied to every job, regardless of size or complexity, is the most common way overhead distorts job-level margin. A $50,000 renovation and a $1.2M commercial fit-out don’t carry the same burden. Applying the same rate to both produces a margin number that’s approximately wrong for each.

What Your Cost Codes Are Actually Capturing (and What They’re Missing)

Direct vs. indirect costs in a cost code structure

A well-structured cost code system tracks labor, materials, equipment, and subcontractors at the line-item level. A flat structure that rolls everything into three or four broad categories tells you what a project cost but not which cost drove the variance. It can’t support the estimate-versus-actual analysis that makes the next bid more accurate.

The standard is a hierarchical structure: parent codes (3000-Framing) with sub-items (3100-Framing Labor, 3200-Framing Lumber).3 That lets you review costs at both a summary and a line-item level. Construction job costing at that granularity is what makes estimates improve over time rather than repeat the same errors.

What happens when equipment and subcontractor costs aren’t coded correctly

Equipment costs, both internal fleet and rental, are frequently miscoded or left uncoded entirely. When a piece of equipment shows up as a general business expense instead of a job-level cost, every project that uses it looks more profitable than it was. Subcontractor invoices have the same problem: coded to the wrong job or to a catch-all expense account, they create a margin gap that doesn’t surface until year-end.

Accurate contractor bookkeeping means someone is reviewing cost code assignments in real time, not catching up at month-end after the project has already moved on.

What Construction Job Costing Misses Without a Monthly WIP Update

How the percentage-of-completion method depends on real-time cost data

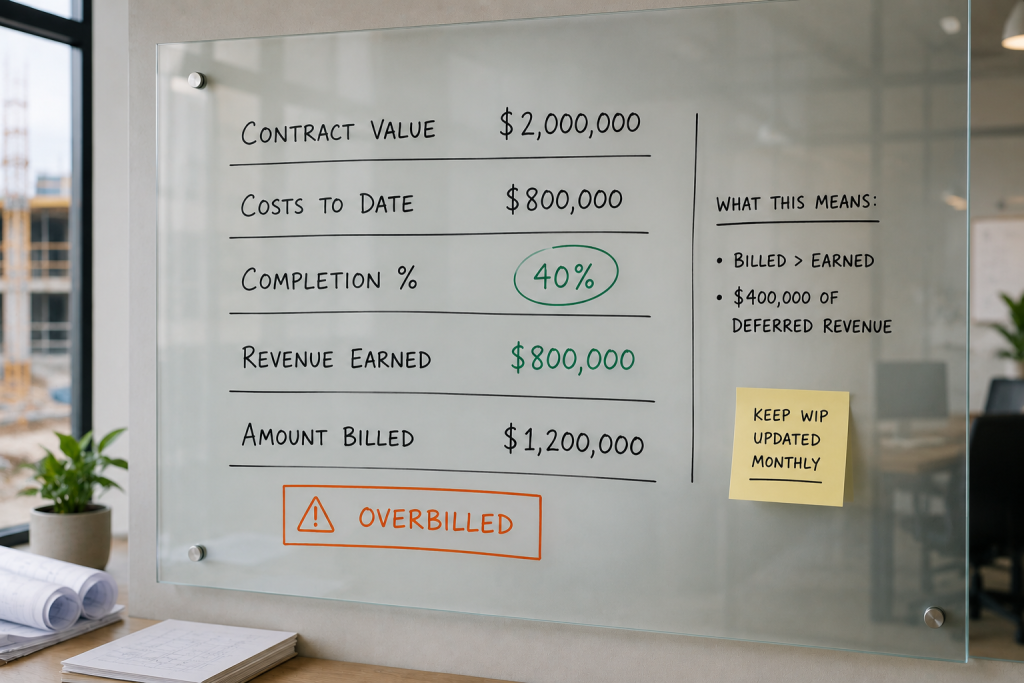

The percentage-of-completion method recognizes revenue based on project completion, not when invoices go out. The standard calculation: costs incurred to date divided by total estimated costs. If a $2M project has $800K in costs recorded, it’s 40% complete, and 40% of the contract value gets recognized as revenue that month.4

That math only works if “costs incurred to date” is accurate. A WIP schedule built on incomplete cost data produces a completion percentage that doesn’t match the actual work done. The financials look clean. The job isn’t.

Overbilling and underbilling — what they signal and why they matter

Overbilled positions appear on the WIP as deferred revenue — money received that hasn’t been earned yet based on completion percentage. Underbilled positions represent earned revenue that hasn’t been billed. Both are normal in construction. Neither should be invisible.

When the WIP schedule isn’t updated monthly, overbilled and underbilled positions accumulate without anyone managing them. A lender reviewing quarterly financials will catch the distortion. A surety company reviewing the WIP before issuing a bond will catch it faster.

How Retainage Distorts Your Cash Position Until It’s Too Late

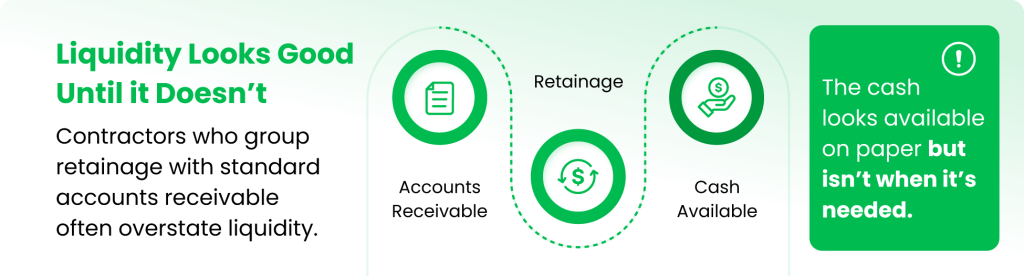

Retainage receivable is an asset, not cash

Retainage is the percentage withheld, typically 5–10% of each progress payment, until contract completion or defined milestones. It’s money earned on work already performed. But it won’t arrive for months, sometimes not until after a final inspection, punch list completion, and signed lien waivers.

How retainage surprises arrive at bonding time

Surety companies and lenders evaluate working capital when underwriting bonds and credit lines. A contractor showing $400K in AR that includes $180K in retainage looks more solvent than the cash position supports. When the surety separates retainage from current AR, bonding capacity comes in lower than expected, typically right when the contractor needs to qualify for the next large job.

When Generic Bookkeeping Creates Job-Level Blind Spots

What construction-fluent bookkeeping actually requires

Standard bookkeeping tracks income and expenses against a chart of accounts. Construction bookkeeping adds a job list, cost code structure, WIP schedule, retainage ledger, and billing schedule to that. All of it updated monthly, all of it tied to the format banks and surety companies use.

Those aren’t the same discipline. A bookkeeper who handles cash-basis accounting for a service business can code transactions accurately and still produce reports that tell a GC nothing useful about job-level profitability. Accurate construction bookkeeping requires someone who understands WIP schedules, percentage-of-completion reporting, and what a bonding agent is actually looking at.

The AIA G702/G703 connection to job cost accuracy

AIA G702 and G703 are the standard payment application forms on most commercial projects.5 They’re also source documents for WIP updates and percentage-of-completion calculations. A bookkeeper who doesn’t understand those forms can’t use them to update the WIP accurately, and the job-cost report drifts further from reality with each billing cycle.

Conclusion

Construction job costing works when three disciplines are in place at once: costs coded to the right job and cost code in real time, a WIP schedule updated every month, and retainage tracked as a separate receivable rather than folded into cash. When any one of these slips, the margin number on the job-cost report stops reflecting what the project actually produced.

Most contractors who lose money on jobs that should have been profitable aren’t missing the right software. They’re missing the accounting discipline to keep the data accurate while the project is running. That’s the gap between a system that shows you what happened and one that shows you what’s happening, while there’s still time to act on it.

To see what that looks like in practice, contact FullStaff to review a sample WIP schedule and job-cost summary we produce monthly for construction businesses.

Frequently Asked Questions (FAQs)

What is construction job costing?

Construction job costing is the process of tracking every cost associated with a specific project — labor, materials, equipment, subcontractors, and allocated overhead — and comparing those actual costs against the original estimate. Unlike standard bookkeeping, which organizes expenses by account category across the whole company, job costing assigns every dollar to a specific project and cost code.

How does job costing differ from standard bookkeeping for contractors?

Standard bookkeeping tracks income and expenses at the company level — useful for tax preparation and year-end financial reporting, but it can’t tell you whether any individual project made money. Job costing adds a project layer to every transaction, attaching each expense to a specific job, cost code, and phase of work. That layering is what makes it possible to compare estimated costs to actual costs on a running basis, catch budget overruns before they compound, and build more accurate estimates for the next bid.

What costs should be included in a construction job cost report?

A complete job cost report captures all direct costs — labor (including burden), materials, subcontractor invoices, and equipment (both rental and company-owned fleet) — along with a proportional allocation of overhead expenses such as insurance, vehicle costs, and office staff. Many contractors track direct costs accurately but skip overhead allocation, which causes every job to appear more profitable than it actually is. The margin number is only reliable when all cost categories are captured and properly assigned.

How often should contractors update their job cost reports?

Monthly at minimum, and more frequently on active projects with significant billing activity. A job cost report updated only at project closeout can’t inform decisions while work is still running. For percentage-of-completion accounting, the monthly WIP schedule depends on cost data being current — which means cost coding and job cost updates need to be part of the regular monthly close process, not a reconciliation exercise after the project has already finished.

What is a WIP schedule and why does it matter?

A work-in-progress (WIP) schedule is a financial report showing the current status of every active contract: costs incurred to date, percentage of completion, revenue earned based on that percentage, total billed to date, and whether each job is overbilled or underbilled. Lenders and surety companies use the WIP schedule to assess financial health and bonding capacity — not the P&L alone. When the WIP isn’t updated monthly, or when it’s built on inaccurate cost data, it misrepresents both individual project status and the overall financial position of the company.

What’s the difference between overbilling and underbilling in construction?

Overbilling means a contractor has invoiced the client for more than the percentage of work actually completed — it creates a liability on the WIP schedule because that revenue hasn’t been fully earned yet. Underbilling is the reverse: work has been completed but not yet invoiced, creating an asset (earned but unbilled revenue). Both are normal in construction. Large or growing overbilled positions are a risk signal to surety companies and lenders; large underbilled positions can mask cash flow problems that compound across multiple billing cycles.

How does retainage affect job costing?

Retainage — typically 5–10% of each progress payment withheld by the project owner until completion — reduces the actual cash received on each billing. For job costing and cash flow purposes, retainage receivable must be tracked separately from standard accounts receivable and excluded from near-term liquidity calculations. A contractor carrying $200K in retainage receivable across active projects does not have that cash available for payroll or materials purchases. Treating retainage as current AR overstates working capital and produces cash flow projections that don’t hold up when the bills come due.

What software do contractors use for job costing?

QuickBooks Online is the most widely used platform for contractor bookkeeping and supports job costing through its Projects feature and cost code structure. Specialty construction platforms — Foundation, Sage 100 Contractor, Procore, and others — offer more native WIP reporting and AIA billing support out of the box. The platform matters less than whether the job costing features are actually configured, cost codes are set up correctly, and someone is coding every transaction consistently. Most job cost problems aren’t software failures — they’re discipline and setup problems that persist regardless of which system is running.

Can AI replace a construction bookkeeper?

AI can automate repetitive accounting tasks — transaction categorization, invoice processing, data entry — but it doesn’t replace the judgment that construction-specific accounting requires. Reviewing a WIP schedule for accuracy, allocating overhead proportionally across projects, separating retainage from current AR, and reconciling AIA billing documents against job cost records all require someone who understands how construction accounting works at a structural level. Most construction businesses use AI tools to reduce transaction volume while keeping a skilled accountant focused on the work that requires interpretation, oversight, and compliance review.

How does job costing affect bonding capacity?

Surety companies evaluate the WIP schedule, financial statements, and working capital position when underwriting bonds. Accurate job costing feeds all three. If job cost records are inconsistent, the WIP schedule is unreliable, retainage is miscategorized, or significant overbilling goes untracked, the financial picture the surety sees doesn’t match the actual risk profile. Contractors with clean, consistent job cost records typically qualify for higher bonding limits because the underwriter can see exactly where the exposure is — and where it isn’t.

Let FullStaff Handle Your Bookkeeping

If your job-cost reports say profitable but your cash account says otherwise, the problem usually lives in one of three places: overhead allocation, retainage tracking, or a WIP schedule that’s running a month behind. Those aren’t software problems. They’re bookkeeping discipline problems, and they compound with every project that closes without accurate numbers behind it.

Since 2012, FullStaff has provided dedicated accounting professionals to construction businesses managing complex, multi-project financials. We handle the books that require construction literacy, not just accounting basics.

- Monthly job cost reporting by project and cost code

- WIP schedule preparation and percentage-of-completion tracking

- Retainage receivable tracking, separate from current accounts receivable

- AIA G702/G703 billing support and reconciliation

- Certified payroll and labor burden allocation

- Monthly close with financial statements ready for lenders and surety companies

Here’s how it works: complete a short kickoff form, meet with our team to review your project mix and current accounting setup, and we match you with a dedicated professional who understands construction accounting from the WIP schedule up.

References:

- What Percentage of Small Businesses Fail?

- Job Costing vs. Guessing: Why 80% of Contractors Fail at Profitable Bidding

- How to Use Cost Codes to Enhance Job Costing in QuickBooks Online

- Percentage of Completion Method Defined With Examples

- A Contractor’s Guide to AIA Billing