Most real estate businesses don’t have a transaction problem—they have a visibility problem. As deals close and commissions come in, commission ledgers, agent splits, trust-account compliance, broker disbursements, and escrow reconciliation can quickly become difficult to manage without the right systems in place.

The challenge isn’t a lack of activity—it’s keeping up with everything happening behind the scenes. When financial tracking falls behind, even a successful month can leave questions about profitability.

The good news is that effective bookkeeping for real estate agents doesn’t have to be complicated. The five essentials below can help create clearer financial visibility, improve accuracy, and support better business decisions.

What Effective Real Estate Bookkeeping Actually Looks Like

According to the National Association of REALTORS®, many real estate professionals operate as independent contractors responsible for managing their own business finances.1 That responsibility requires clear financial records.

Effective real estate bookkeeping includes:

- Maintaining a detailed commission ledger

- Reconciling agent splits consistently

- Separating trust accounts from operating accounts

- Tracking expenses by meaningful categories

- Reviewing financial reports monthly

- Maintaining clean tax documentation

- Monitoring transaction-level profitability

The challenge is consistency, not complexity.

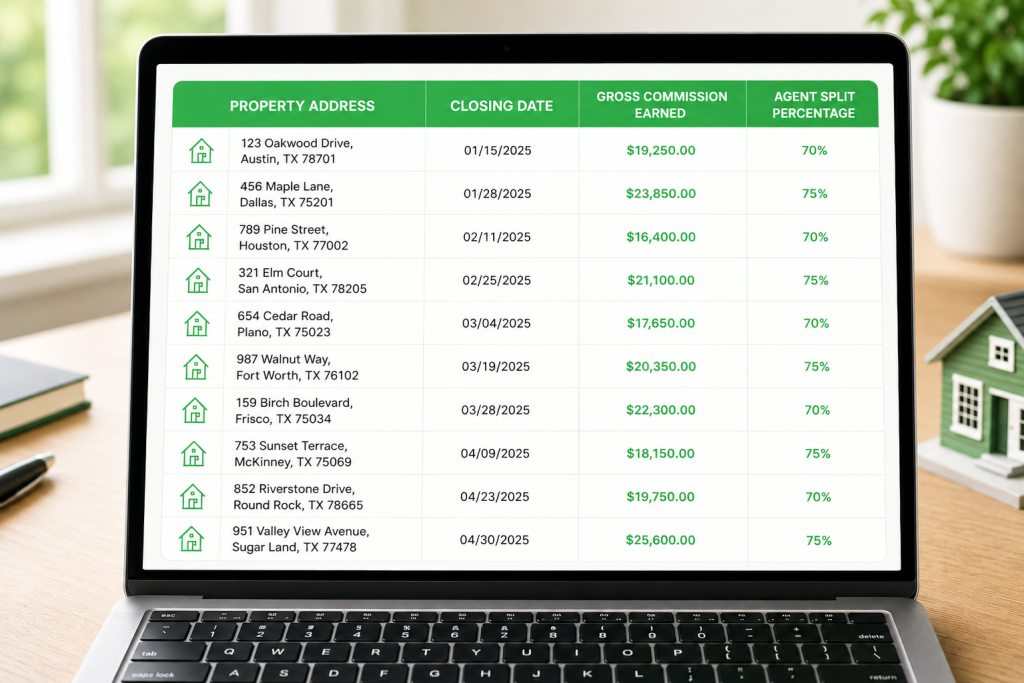

1. Keep a Detailed Commission Ledger

Every transaction creates multiple financial entries. Gross commissions, referral fees, agent splits, brokerage retention, transaction expenses, and final payouts all need to be tracked accurately.

Many real estate businesses begin with spreadsheets that work well when transaction volume is low. As more agents, listings, and closings enter the picture, those systems become harder to maintain. Small mistakes become easier to miss.

A commission ledger should include:

- Property address

- Closing date

- Gross commission earned

- Agent split percentage

- Referral fees

- Brokerage retention

- Net payout amount

- Payment status

This level of detail allows brokerages to verify that every transaction has been processed correctly. It also provides a reliable audit trail when questions arise months later.

📊 Accurate commission tracking remains critical in real estate, where many professionals operate as independent contractors under the IRS’s independent contractor classification guidelines.2

A strong commission ledger does more than track income. It creates accountability throughout the entire transaction process.

2. Separate Trust Accounts from Operating Funds

| Trust Account |

| Client Funds |

| Escrow Deposits |

| Earnest Money |

| Reconcile Monthly |

| Operating Account |

| Business Income |

| Business Expenses |

| Profit & Loss Tracking |

| Budgeting & Planning |

Note: Keep client fund in Trust Account. Keep business income and expenses in the Operating Account.

One of the most important aspects of bookkeeping for real estate agents is maintaining strict separation between trust funds and operating funds.

Client money should never be treated the same way as business operating cash. Escrow deposits, earnest money, and other client-held funds require separate tracking and reconciliation procedures.

Trust-account management isn’t simply a bookkeeping preference. In many states, it is a compliance requirement. Failing to maintain accurate records can create regulatory issues that extend far beyond bookkeeping.

Monthly trust-account reviews should include:

- Bank reconciliation

- Escrow balance verification

- Outstanding deposit review

- Transaction matching

- Documentation retention

The National Association of REALTORS® Code of Ethics emphasized that real estate professionals have fiduciary responsibilities that include the proper handling of client funds.3 Trust-account issues often begin as small reconciliation discrepancies. Left unresolved, they can become much larger problems.

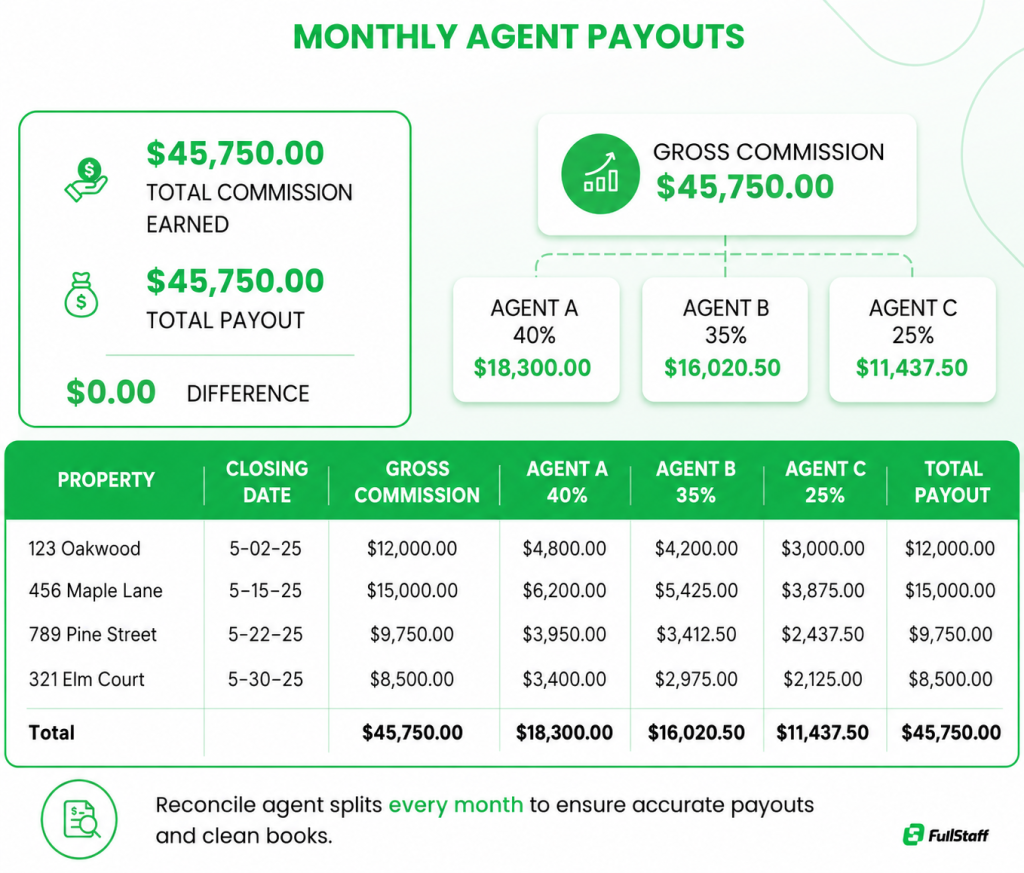

3. Reconcile Agent Splits Every Month

Few industries deal with compensation structures as frequently as real estate.

Some agents work under fixed commission arrangements. Others operate under graduated splits, team agreements, production incentives, referral partnerships, or brokerage caps. Every variation increases the complexity of financial tracking.

This is where many firms begin to see the value of specialized real estate bookkeeping services.

Monthly reconciliation helps ensure:

- Agents receive accurate payouts

- Brokerage revenue is reported correctly

- Referral fees are allocated properly

- Contractor payments remain accurate

- Financial reports reflect actual performance

The Internal Revenue Service emphasizes the importance of maintaining complete financial records through its IRS Recordkeeping Guide.4 Accurate records support tax compliance while also improving financial visibility throughout the year.

Many payout disputes begin with a simple bookkeeping error that remains unnoticed for months.

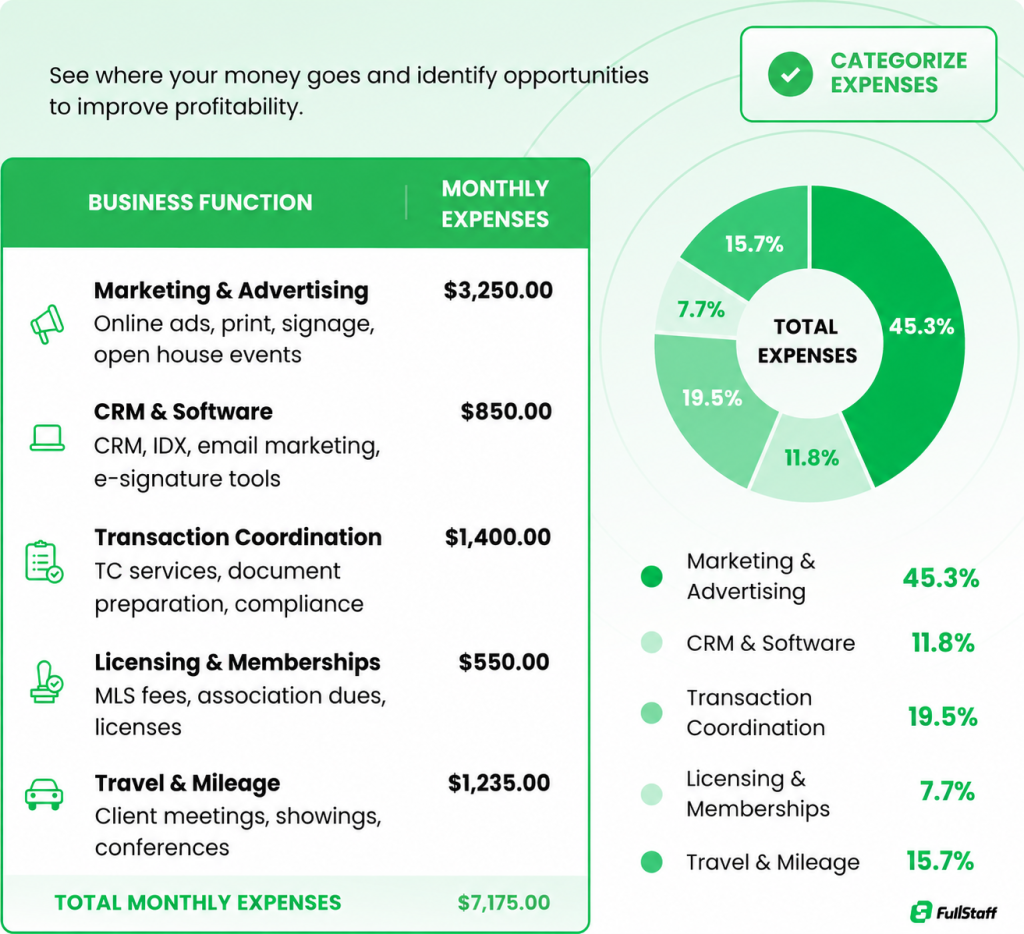

4. Track Expenses by Business Function

Many real estate businesses track expenses at a high level. Marketing, software subscriptions, transaction coordination, licensing fees, and travel expenses often get grouped into broad categories that provide little operational value.

The problem is that broad categories make it difficult to identify what is actually driving profitability. A brokerage may spend heavily on lead generation while seeing minimal returns, but the issue remains hidden when all marketing-related costs are grouped together.

Strong real estate bookkeeping separates expenses into meaningful categories that support decision-making.

Common expense categories include:

- Digital advertising

- Lead generation platforms

- CRM subscriptions

- MLS fees

- Professional memberships

- Continuing education

- Vehicle and travel expenses

- Office and administrative expenses

- Transaction coordination services

Categorizing expenses this way helps identify which activities contribute to growth and which create unnecessary overhead.

📊 The U.S. Small Business Administration emphasizes the importance of maintaining organized financial records to evaluate performance and support business planning.5

Detailed expense tracking also makes budgeting easier. Instead of reacting to rising costs after the fact, brokerages can identify trends before they become significant financial issues.

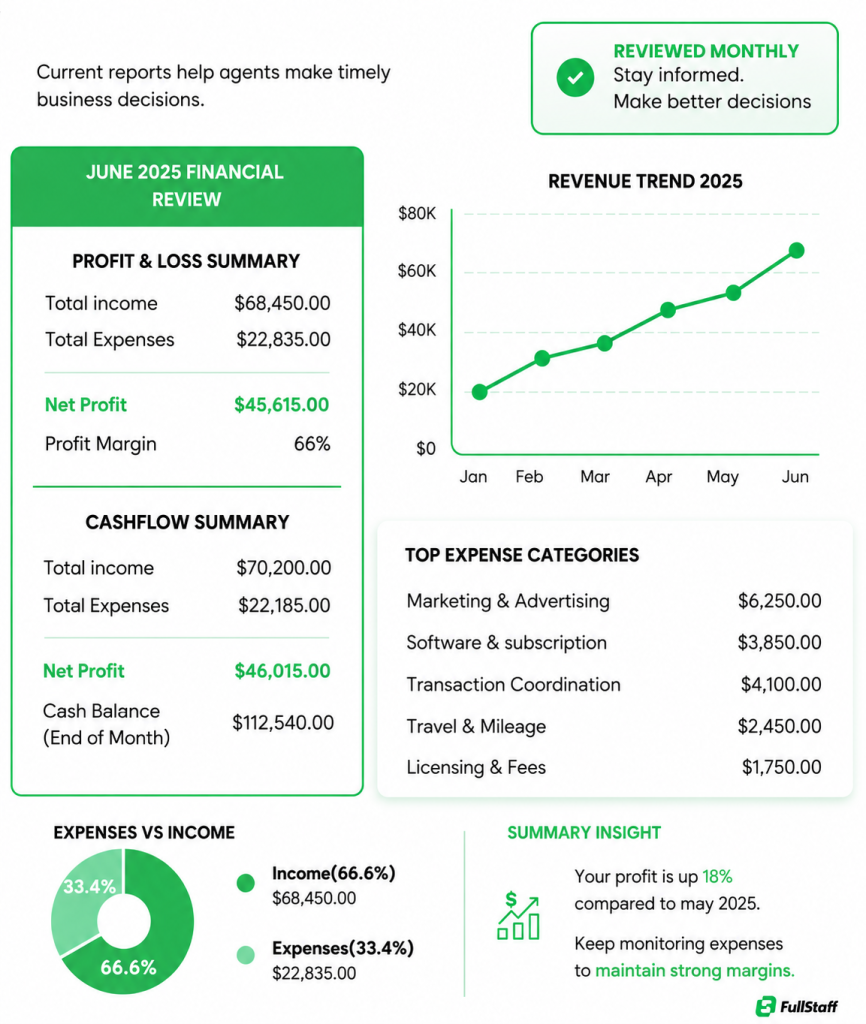

5. Review Financial Reports Every Month

Many agents only review financial statements when preparing taxes. By that point, the information is often several months old and less useful for making operational decisions.

Monthly reporting creates visibility while there is still time to respond. Regular reviews can help identify profitability trends, monitor cash flow, and uncover issues before they affect the business.

At a minimum, real estate businesses should review:

- Profit and loss statements

- Balance sheets

- Cash flow summaries

- Commission income reports

- Expense breakdowns

- Accounts receivable reports

These reports provide a clearer picture of overall business performance. They help answer important questions about profitability, cash flow, and growth.

📊 As mentioned in QuickBooks’ guide to financial statements for small business owners, reviewing key reports such as the balance sheet, income statement, and cash flow statement helps business owners better understand financial performance and profitability.6

The value of financial reports comes from timing. Reports generated months after decisions are made have limited usefulness.

Why Bookkeeping for Real Estate Agents Matters

As a real estate business grows, bookkeeping becomes more specialized. Commission reconciliation, trust-account reporting, contractor payments, and compliance tracking can quickly outgrow manual processes.

Many firms turn to real estate bookkeeping services to improve accuracy, maintain visibility, and support growth without adding administrative burden. Accurate commission tracking, trust-account management, agent split reconciliation, expense categorization, and monthly financial reporting all contribute to a clearer understanding of business performance.

📊 Accurate financial records help business owners monitor cash flow and understand profitability, as highlighted in Xero’s guide to small business bookkeeping.7

Real estate businesses generate large volumes of financial activity. Without strong bookkeeping systems, important details become difficult to track, profitability becomes harder to measure, and decision-making becomes less reliable.

Effective bookkeeping for real estate agents is about much more than preparing for tax season. The firms that scale successfully aren’t always the ones closing the most transactions—they’re often the ones with the clearest understanding of their numbers.

Frequently Asked Questions (FAQs)

How does bookkeeping work for real estate agents?

Bookkeeping for real estate agents involves recording, organizing, and reconciling commissions, expenses, agent payouts, and other financial transactions to maintain accurate records and support informed business decisions.

Why is commission tracking important in real estate?

Commission tracking helps ensure that agents, brokers, and referral partners receive accurate payments while providing a reliable record of revenue and profitability. It also helps identify discrepancies early and supports more accurate financial reporting.

What is a commission ledger?

A commission ledger is a detailed record of each transaction’s commission income, agent splits, referral fees, brokerage retention, and final disbursements. It helps ensure commissions are tracked accurately and provides a clear audit trail for financial reporting.

How often should real estate books be reconciled?

Most real estate businesses should reconcile bank accounts, trust accounts, and commission records monthly to maintain accurate financial reporting and identify discrepancies early. Regular reconciliations can also help prevent errors from carrying over into future reporting periods.

What expenses should real estate agents track?

Agents should track marketing expenses, software subscriptions, MLS fees, travel costs, licensing expenses, professional dues, and transaction-related services. Categorizing these expenses properly can help improve budgeting, monitor profitability, and simplify tax preparation.

Why is trust-account reconciliation necessary?

Trust-account reconciliation helps ensure that client funds remain properly separated from business operating funds while supporting compliance and financial accuracy. Regular reconciliation can also help identify discrepancies before they become larger financial or regulatory issues.

What financial reports should real estate agents review monthly?

Agents should review a profit and loss statement, balance sheet, cash flow report, commission activity report, and expense summary every month. Together, these reports provide a clearer picture of profitability, financial health, and overall business performance.

What are real estate bookkeeping services?

Real estate bookkeeping services provide specialized financial support for commission tracking, reconciliations, reporting, compliance documentation, and ongoing bookkeeping management. They help agents and brokerages maintain accurate records while improving financial visibility.

Can bookkeeping help reduce tax-time stress?

Yes. Consistent bookkeeping creates organized records throughout the year, making tax preparation more efficient and reducing the likelihood of errors or missing documentation. It can also make it easier to identify deductions and provide supporting records when needed.

Can AI replace a real estate bookkeeper?

AI can automate repetitive tasks such as data entry and transaction categorization, but human bookkeepers remain essential for interpreting financial information, resolving discrepancies, ensuring compliance, and providing professional judgment. The most effective approach often combines automation with experienced oversight.

Let FullStaff Handle Your Bookkeeping

Real estate businesses face financial challenges that generic bookkeeping often overlooks. Commission tracking, trust-account compliance, escrow reconciliation, and agent split management all require specialized attention.

Since 2012, FullStaff has helped businesses build dedicated accounting support teams that improve financial visibility while reducing administrative workload.

Our real estate bookkeeping support includes:

- Commission ledger tracking

- Agent split reconciliation

- Trust-account reporting

- Escrow reconciliation support

- Monthly bank and credit card reconciliation

- Financial statement preparation

- Accounts payable and receivable support

Here’s how it works:

- Complete a short kickoff form.

- Meet with our team to discuss your bookkeeping needs.

- Get matched with a dedicated accounting professional who works as an extension of your business.

References:

- Highlights from the NAR Member Profile

- Independent contractor defined

- NAR The Code of Ethics

- IRS Recordkeeping Guide

- U.S. Small Business Administration – Manage Finances

- Financial Statements: A guide for Small Business Owners

- Small business bookkeeping: beginner’s guide and tips