Dentrix or Open Dental can tell you what the practice produced last month, by provider and procedure. Most bookkeeping can’t show what happened next: how much was adjusted, what’s still waiting on EOBs, and how much actually reached the bank. That’s the production–collections gap, and tax-focused books can’t see it.

The gap is rarely dramatic. Production looks fine, deposits arrive, the CPA files on time. What’s missing is the connection between the three.

That difference between what a practice produces and what it collects is where a bookkeeping system earns its keep, or doesn’t. The rest of this article covers what bookkeeping for dental practices should include, component by component, and the practice decision each one supports.

Essential Features of Bookkeeping for Dental Practices

| A dental-specific chart of accounts that separates income by provider type and expenses into dental categories |

| A monthly reconciliation of production in the practice management system against collections in the books |

| Insurance AR tracking, with EOB payments allocated correctly and claim aging reviewed on a schedule |

| Expense tracking measured against dental overhead benchmarks, not generic small-business ratios |

| Payroll handled as the largest expense line, with provider compensation kept separate from staff costs |

| A monthly close that produces reports a practice owner can act on |

| Recordkeeping and internal controls that satisfy the IRS and make theft harder to hide |

None of this is complex. The challenge is that most books are set up for the tax return, not the practice.

Why the Bank Balance Can’t Tell You If the Practice Is Profitable

A generic chart of accounts puts every deposit into one income line and sorts expenses into buckets designed for any small business. The books balance, the return gets filed, and no one can answer a basic question: is hygiene carrying its weight, and where did the write-offs go?

Bookkeeping for dental practices starts with a chart of accounts built for the industry. Income is separated by source, while dental-specific expenses like supplies, lab fees, and payroll are tracked separately for clearer financial insights.

The same logic applies to reductions in revenue. An insurance adjustment off a contracted fee schedule, a courtesy discount, and an uncollectible balance are three different problems. Books that lump them into one “write-off” line hide which one is growing.

Production Isn’t Revenue Until It Clears the Bank

The practice management system reports production. The bank reports deposits. In many practices, nobody reconciles the two, so the collection rate (collections divided by production) is a number the owner feels rather than tracks.

This reconciliation should happen monthly, not just at year-end. The books should match collections to adjusted production, with any gap explained by insurance in process, patient balances, or adjustments. An unexplained gap is often the first sign of billing issues.

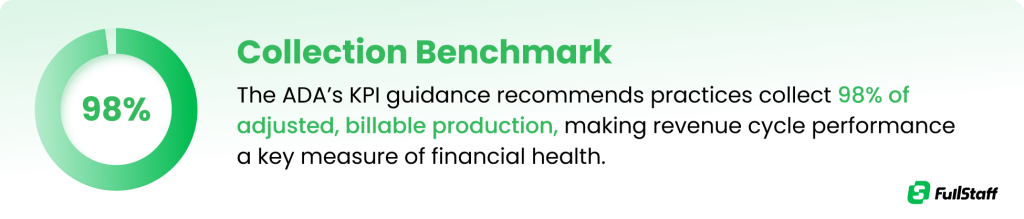

Against that 98% benchmark, an 84% collection rate isn’t a rounding error.1 On $1.2M of adjusted production, every point of slippage is $12,000 that was earned and never collected. Bookkeeping for dentists exists, in large part, to make that number visible every month instead of once a year.

Insurance AR Ages Faster Than You Think

A claim can take anywhere from two weeks to two months to pay, and it can come back denied for reasons that have nothing to do with clinical judgment.

That has a direct bookkeeping consequence. The books need an insurance AR aging that someone reviews on a schedule, because a denied claim that sits for 60 days often becomes a write-off by default. Each EOB also has to be posted correctly, allocated to the right procedures and providers, with the insurance adjustment recorded as an adjustment rather than quietly absorbed.

Sloppy EOB posting corrupts everything downstream. Provider production reports drift from reality, the collection rate loses meaning, and the adjustments line stops being trustworthy.

Where Overhead Hides When Expenses Are Categorized Wrong

Dental overhead has established benchmarks, making it easier to measure practice performance. Most practices spend 60% to 65% of collections on overhead,2 with dental supplies averaging 6% and lab fees 8%, or 2–3% for practices using CAD/CAM.

Benchmarks only work when expenses are categorized correctly. A payment to a dental supplier may include supplies, repairs, and equipment. If it’s all recorded as “dental supplies,” the numbers become misleading. That’s a common dentist bookkeeping mistake that hides the real source of costs.

Done right, bookkeeping for dental practices turns the P&L into a scorecard: each major category carries a target percentage of collections, and drift gets caught in a month rather than discovered at year-end.

Payroll Is the Largest Line and the Easiest to Misread

Staff costs are the biggest expense in nearly every practice, and the benchmark is specific: total employee costs at or below 28% of collections, with a goal of 24–26%. That figure includes payroll taxes, retirement contributions, and benefits, not just wages.

The common distortion is putting associate compensation in staff costs. Provider pay belongs with owner compensation, not team payroll; blend them and the staff-cost ratio looks alarming while telling you nothing. The books should also split payroll by department (chairside, front desk, hygiene) so a rising ratio points somewhere specific.

Clean Records Are Also Your First Theft Control

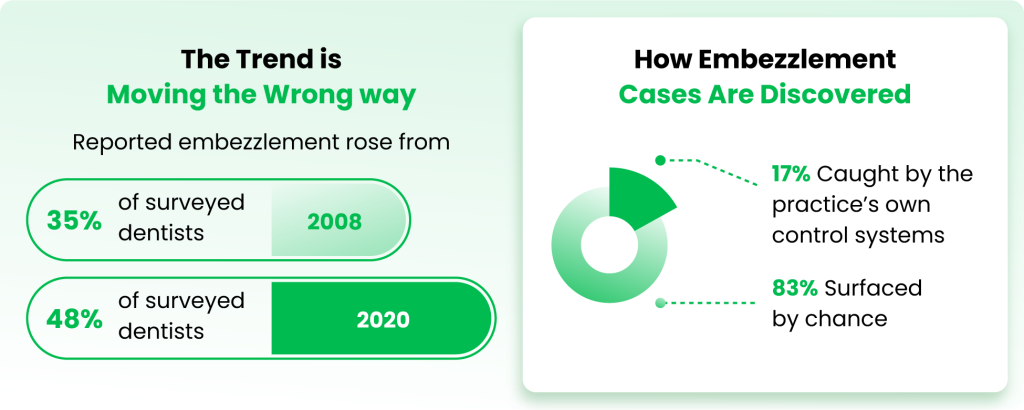

Dental practices are small, trusting workplaces where one person often handles scheduling, payments, and adjustments. That’s exactly the environment where theft goes unnoticed.

📊 Nearly 49% of dental practices have experienced employee theft, and nearly 46% of those more than once.3

Bookkeeping for dental practices is the control system that’s supposed to do that job. Daily reconciliation of the day sheet against the actual deposit, separation of duties so the person posting payments isn’t the person reconciling the bank, and a monthly review of the adjustments report close the most common openings.

None of this requires suspicion of anyone. It requires a system where the numbers get checked by someone other than the person who entered them.

Monthly Reporting Turns Dentist Bookkeeping Into a Management Tool

Everything above feeds one deliverable: a monthly close, finished by a fixed date, that produces reports worth reading. Three cover most of what an owner needs: a P&L in dental categories with each line shown as a percentage of collections, the production-to-collections reconciliation, and the insurance AR aging.

That package takes about 20 minutes a month to review, and it changes the questions an owner can ask. Instead of “can we afford it?”, the conversation becomes “supplies ran 8% against a 6% target, so what was in that order?” Bookkeeping built specifically for dental practices is what makes that conversation possible, because the categories, benchmarks, and reconciliations are already in place.

Books that close in January answer January’s questions in March. Books that close by the 10th answer them while the schedule can still be changed.

Conclusion

Bookkeeping for dental practices should include a dental chart of accounts, a monthly production-to-collections reconciliation, insurance AR tracking, benchmarked expense categories, clean payroll, and a close that ships on a fixed date.

Two takeaways matter most. First, the tax return is a byproduct of good books, not the purpose of them; the purpose is answering practice questions while they’re still decisions. Second, benchmarks only mean something when the categorization underneath them is right, so precision in the boring work is what makes the reports trustworthy.

If your current books can’t explain last month’s production–collections gap, ask to see a sample EOB reconciliation and month-end report package for a practice your size. It makes the difference concrete faster than any article can.

Frequently Asked Questions (FAQs)

What does bookkeeping for a dental practice include?

Dental practice bookkeeping includes a dental-specific chart of accounts, monthly reconciliation of production against collections, insurance AR and EOB payment tracking, expense categorization measured against dental overhead benchmarks, payroll with provider compensation separated from staff costs, and a monthly close with financial reports. The distinguishing feature is the connection to the practice management system: the books should explain the gap between what was produced and what was collected.

What is the difference between production and collections in dental bookkeeping?

Production is the value of dentistry performed, recorded in the practice management system; collections are the payments actually received from patients and insurers. Adjusted production subtracts contracted write-offs from gross production, and the collection rate (collections divided by adjusted production) measures how much earned revenue reaches the bank. The ADA’s benchmark is collecting 98% of adjusted production.

Should dental practices use cash or accrual accounting?

Most dental practices keep their books on a cash or modified-cash basis, which is simpler and usually advantageous for tax purposes. The practice-management picture that accrual would provide (production earned but not yet collected) typically comes from pairing cash-basis books with the practice management system’s production and AR reports rather than converting to full accrual. The right choice depends on entity structure and revenue, so confirm it with your CPA.

What percentage of collections should dental practice overhead be?

Typical dental practice overhead runs 60–65% of collections, and the ADA’s guidance treats 63% or less as healthy. Within that total, common benchmarks are dental supplies around 6%, lab fees around 8%, and total staff costs at or below 28% of collections. Overhead consistently above 70% usually signals either a cost problem or a collections problem masquerading as one.

What is a dental-specific chart of accounts?

A dental-specific chart of accounts is the account structure that organizes a practice’s books around dental operations rather than generic business categories. Income is separated by provider type and payment source, expenses carry dedicated lines for dental supplies, lab fees, and departmental payroll, and revenue adjustments distinguish insurance write-offs from discounts and bad debt. It’s what allows the P&L to be compared against dental benchmarks.

How often should a dental practice reconcile its books?

Bank and credit card accounts should be reconciled monthly at minimum, and the day sheet should be matched to the actual deposit daily. The monthly close (reconciliations plus the production-to-collections tie-out) should finish by a fixed date, ideally around the 10th, so reports arrive while the month they describe is still recent enough to act on.

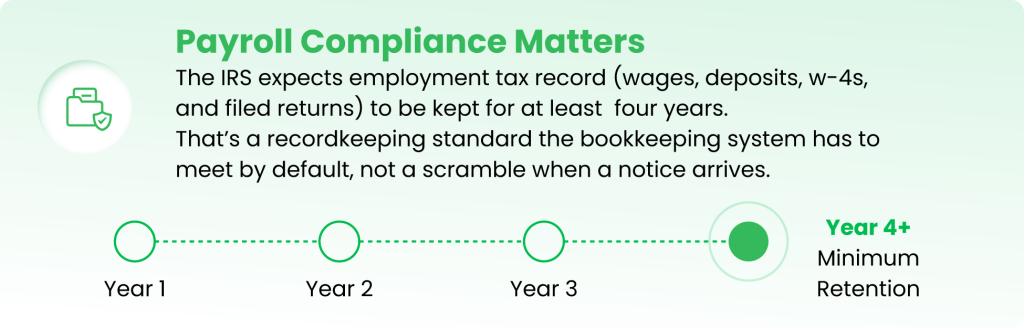

How long do dental practices need to keep payroll and tax records?

Employment tax records must be kept for at least four years after the tax is due or paid, and general business tax records for at least three years, with longer periods in specific situations, such as six years if income is substantially underreported. For a dental practice, that means payroll registers, deposit confirmations, W-4s, and filed returns need organized, retrievable storage as a routine part of the bookkeeping system.

Do dentists need a bookkeeper who knows dental?

A bookkeeper who knows dental will set up the chart of accounts around production types, post EOBs correctly, and grade expenses against dental benchmarks: three things a generalist typically won’t do without direction. A generalist can keep accurate books, but accuracy isn’t the standard that matters; usefulness is. The test is whether the monthly reports can explain the production–collections gap without extra homework.

Can AI replace a bookkeeper for a dental practice?

AI can automate the repetitive layer of dental bookkeeping (transaction categorization, invoice capture, and parts of reconciliation), but it doesn’t replace a professional for EOB interpretation, adjustment review, benchmark analysis, and judgment calls about what a variance means. Most practices get the best result using AI to compress the data-entry work while an experienced bookkeeper or accountant owns the review, the close, and the reporting.

Let FullStaff Handle Your Bookkeeping

If your books can’t explain where last month’s production went, that’s a fixable problem, and you can see the fix before you commit. Ask for a sample EOB reconciliation and month-end report package for a practice your size.

Since 2012, FullStaff has provided US businesses with dedicated accounting professionals: degreed accountants who work to US GAAP standards and are assigned to your practice, not rotated across a client pool.

- Production and collections reconciliation, tied to your practice management system

- EOB tracking and insurance payment allocation

- Provider-level production reporting

- Bank and credit card reconciliation

- Monthly close with dental-category P&L reporting

Here’s how it works: complete a short kickoff form, meet with our team to define the scope, and get matched with a dedicated accounting professional who learns your practice.

References:

- ADA Measuring Success

- Dental Practice Overhead: Cost Breakdown, Benchmarks, and Insights

- Nearly half of dental practices experience theft from staff